Forums » News and Announcements

Liquid Biopsy Market Growth Opportunity And Forecast to 2032

-

Liquid biopsy has a critical role in the precision medicine approach, as it confirms the safe and effective application of targeted therapeutics. A liquid biopsy helps physicians to analyze tumor-related information through a simple blood test. As researchers are generating data that have the potential to lead to unprecedented biological insight, albeit at the cost of the greater complexity of data analysis. Increasing investments in RD of liquid biopsy products and services and various research fundings is one of the major opportunities in the global liquid biopsy market.

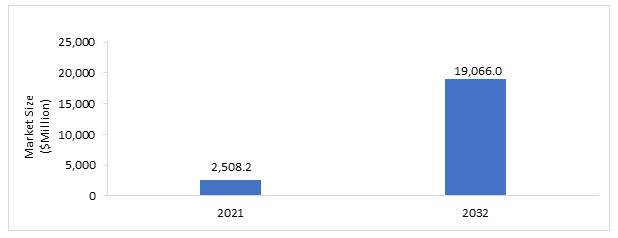

The global liquid biopsy market was estimated to be at $2,508.2 million in 2021, which is expected to grow with a CAGR of 19.83% and reach $19,066.0 million by 2032. The growth in the global liquid biopsy market is expected to be driven by increasing adoption of NGS in various research fields, advancement in NGS, and increase in the adoption of personalized medicine.

Impact of COVID-19

The current global liquid biopsy market comprises various indications such as lung cancer, breast cancer, prostate cancer, and many others. It has been noticed that there has been a reduction in the capacity or shutdowns of laboratories and other research institutions, which have led to reduced usage of various products and services related to research.

The decline in revenues was mostly a result of the initial phases of the COVID-19 pandemic, which comprised complete lockdowns across countries and major cities, thus interrupting the supply chain. The timeline of impact spanned the end of the first quarter and the second quarter of 2020 for most key markets across the globe. However, the pandemic has played a key role in enhancing the growth prospects of liquid biopsy and is expected to indirectly aid in improving the market growth outlook.

Market Segmentation:

Segmentation 1: by Offering

• Testing Service

• Kits

• Platform

• Other ConsumablesThe testing service segment accounted for the largest value, holding $1,169.2 million of the market in 2021. This trend is expected to increase during the forecast period, 2022-2032. As a result of growing awareness among the general population, coupled with the increasing prevalence of cancers and other non-oncology indications, there are tremendous growth opportunities in this segment.

Segmentation 2: by Technology

• NGS

• PCR

• Other Technologies

• Emerging TechnologiesThe largest share can be attributed to the fact that most of the liquid biopsy services and associated kits in the market are based on NGS. It is anticipated that the NGS segment will grow significantly during the forecast period, 2022-2032.

Segmentation 3: by Workflow

• Sample Preparation

• Library Preparation

• Sequencing

• Data Analysis and ManagementAmong all four segments of workflow, the library preparation segment accounted for the largest share, holding 41.18% of the market in 2021. This trend is expected to decline slightly, owing to the entry of novel sequencing platforms in the market during the forecast period (2022-2032). The existing dominance of this segment is primarily attributed to several library preparation kits that are being offered by liquid biopsy key players in the market.

Segmentation 4: by Circulating Biomarkers

• Circulating Tumor Cells (CTCs)

• Cell-Free DNA (cfDNA)

• Circulating Cell-Free RNAs

• Exosomes and Extracellular Vesicles and Others

• Other Circulating BiomarkersThe cell-free DNA segment accounted for the largest share, holding 56.95% of the market in 2021. This existing dominance of cell-free DNA is expected to decline during the forecast period 2022- 2032, with the segment holding an estimate of 56.10% share in 2032 . As a result of growth in clinical applications, the overall biomarker segment is expected to exhibit tremendous growth through the forecast period.

Segmentation 5: by Indication

• Lung Cancer

• Breast Cancer

• Prostate Cancer

• Colorectal Cancer

• Melanoma

• Other Types of Cancer

• Non-Oncology DisorderThe lung cancer segment accounted for the largest share, holding 28.47% of the market in 2021. The existing dominance of this segment is mainly attributed to several higher prevalence of lung cancer coupled with the existing availability of multiple LDT and few approved liquid biopsies in the market.

Segmentation 6: by Clinical Application

• Treatment Monitoring

• Prognosis and Recurrence Monitoring

• Treatment Selection

• Diagnosis and ScreeningThe treatment monitoring segment accounted for the largest share, holding 46.50% of the market in 2021. The existing dominance of this segment is mainly attributed to the availability of multiple treatments monitoring liquid biopsies that are currently offered by key players for different cancer.

Segmentation 7: by Usage

• Clinical

• ResearchThe research segment accounted for the largest share of 66.43% of the market in 2021. The share is expected to decline slightly during the forecast period, 2022-2032. The dominance of the provider segment is attributed to the existing availability of multiple research kits and assay of the key players in the liquid biopsy market.

Segmentation 8: by End User

• Academic and Research Institutions

• Clinical Laboratories

• Pharmaceutical and Biotechnology Companies

• Other End UsersThe academic and research institutions segment dominates the global liquid biopsy market. Academic and research institutions are among the primary end users of liquid biopsy. Research organizations constitute integral facilities for companies as well as independent academic research facilities.

Segmentation 9: by Sample

• Blood

• Urine

• Saliva

• OthersThe blood segment accounted for the largest share, holding 89.90% of the market in 2021. This trend is expected to decline slightly during the forecast period, 2022-2032, with the segment estimated to hold an 89.45% share in 2032. It is expected that other sample type-based liquid biopsy will enter the market during the forecast period, and due to this, a very slight decline in the blood-based liquid biopsy segment is expected.

Segmentation 10: by Region

• North America

• Europe

• Asia-Pacific

• Latin America and Middle East

• Rest-of-the-WorldThe North America region is expected to dominate the global liquid biopsy market during the forecast period 2022-2032. North America has a high adoption rate of liquid biopsy. Backed by several healthcare companies working in the marketplace, the U.S. has the highest implementation of PCR, NGS, and other technologies.

Demand – Drivers and Limitations

Following are the demand drivers for the liquid biopsy market:

• Rising Cancer Prevalence

• Increasing Adoption of Inorganic Growth Strategies in the Market

• Increase in Research Funding from National Cancer InstituteThe market is expected to face some limitations too due to the following challenges:

• Uncertain Reimbursement and Regulatory Policies

• Expected Implementation of Patient Protection and Affordable Care Act in the U.SRecent Developments in the Global Liquid Biopsy Market

• Product Launch in 2020: Sysmex Corporation launched liquid biopsy RUO kits in EMEA region. The kits name is Plasma-SeqSensei, and it is used for non-small cell lung cancer (NSCLC), melanoma, and thyroid cancer.

• Partnership: In 2021, Illumina, Inc. collaborated with Bristol Myers Squibb to innovate and enhance companion diagnostics for therapy selection to further precision oncology. TSO 500 ctDNA is one of the first liquid biopsy assays to enable comprehensive genomic profiling for therapy selection.

• Collaboration: In 2021, QIAGEN collaborated with Sysmex Corporation for the development and commercialization of cancer companion diagnostics using NGS and Plasma-Safe-SeqS technology.Key Market Players and Competition Synopsis

The companies that are profiled have been selected based on inputs gathered from primary experts and analyzing company coverage, product portfolio, and market penetration.

The top segment players include liquid biopsy manufacturers and service providers that capture around 95% of the presence in the market.

Some of the prominent names established in this market are:

• Abcodia Ltd.

• Bio-Rad Laboratories, Inc.

• Biocept, Inc.

• Dxcover Limited

• Elypta

• Epic Sciences

• F. Hoffmann-La Roche Ltd

• Guardant Health

• Illumina, Inc.

• Laboratory Corporation of America Holdings

• LungLife AI, Inc.

• Micronoma

• Natera, Inc.

• Neogenomics Laboratories

• PerkinElmer Inc.

• QIAGEN

• Sysmex Corporation

• Thermo Fisher Scientific Inc.Get Free Sample Report - https://bisresearch.com/requestsample?id=1303type=download

How Can This Report Add Value to an Organization?

Product/Innovation Strategy: Product launches and upgrades in the liquid biopsy industry are aimed at advancing the overall technologies in the market to ensure efficient detection of various applications such as treatment monitoring and treatment selection. Several companies, including Illumina, Inc. and NeoGenomics Laboratories, were involved in product innovations.

Competitive Strategy: Enterprises led by the market juggernauts frequently update their product portfolios with innovative and application-specific products to sustain current market competition. Moreover, a detailed competitive benchmarking of the players operating in the global liquid biopsy market has been done to help the reader understand how players stack against each other, presenting a clear market landscape. Additionally, comprehensive competitive strategies such as partnerships, agreements, and collaborations will aid the reader in understanding the untapped revenue pockets in the market.

BIS Related Studies

NGS Sample Preparation Market - A Global and Regional Analysis